The Importance of Future Planning for a Loved One With Special Needs

By Joanne Marcus, MSW, Executive Director of Commonwealth Community Trust (CCT)

This is the first article in a two-part series discussing Pooled Special Needs Trusts (PSNTs) and Medicare Set-Aside (MSA) accounts. This article will present an overview of PSNTs, their benefits, how to set up a PSNT for a client with special needs, and what to do for clients who also need an MSA.

Understanding PSNTs

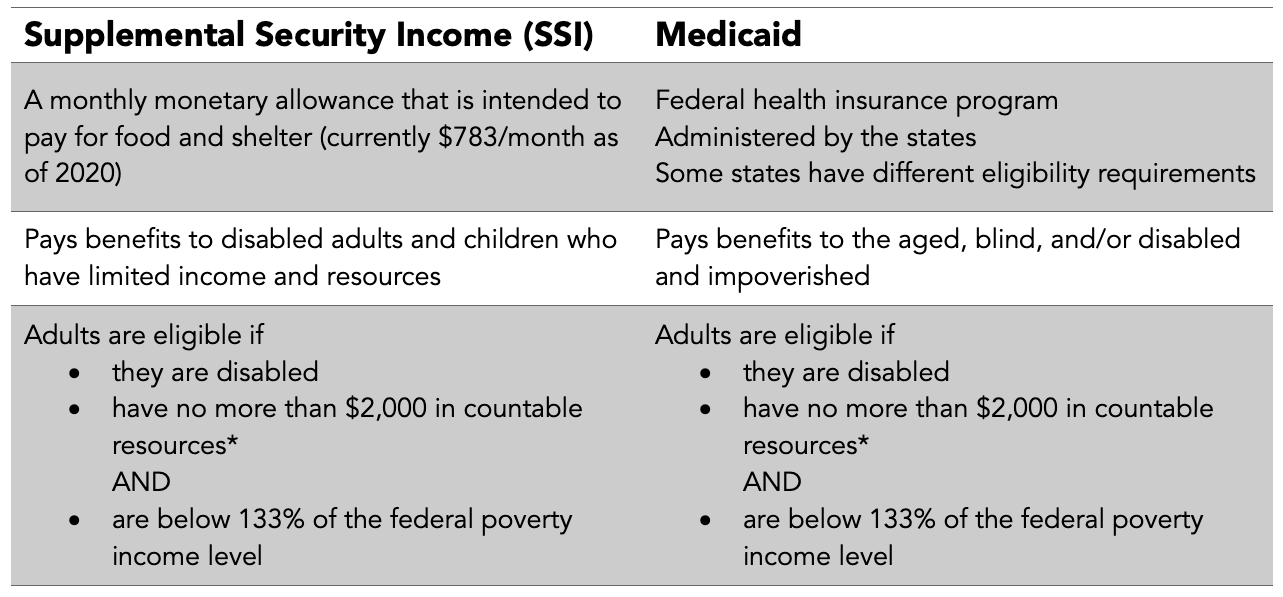

A PSNT is administered by a nonprofit organization that manages and invests funds for individuals with special needs. Distributions are made from the trust to purchase goods and services that supplement public benefits and enhance the beneficiary’s quality of life. All beneficiaries must have a disability, but not all beneficiaries receive public benefits. In some instances, a PSNT is a good option for beneficiaries who simply cannot manage their own financial affairs. Funds placed in a PSNT are not countable resources and do not affect eligibility for means-tested benefits such as Supplemental Security Income (SSI) and Medicaid. Failure to consider a client’s means-tested benefits can result in a malpractice claim, a breach of fiduciary duty, or a dereliction of duty.

The following chart provides key information about Medicaid and SSI:

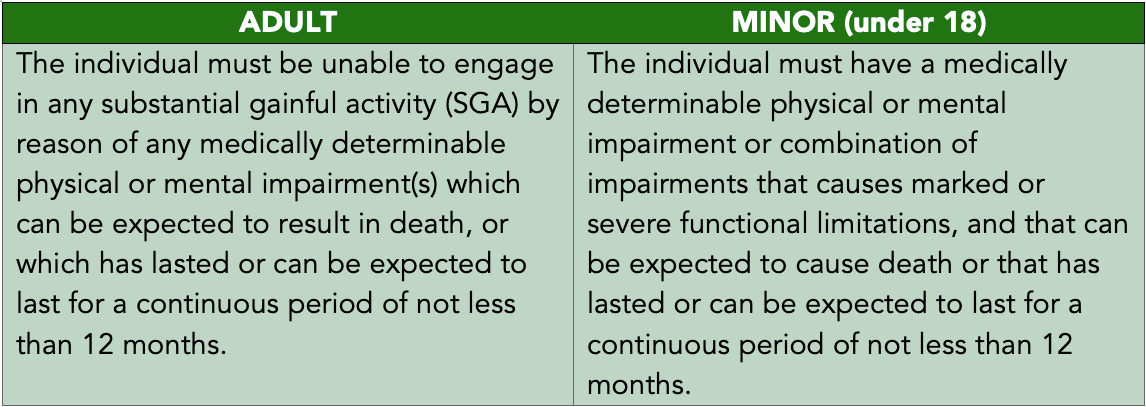

Clients may receive SSI, Medicaid, Medicare, Social Security Disability Insurance (SSDI), or a combination of benefits. The important consideration is that the individual has a disability. The following chart describing SSA’s definition of disability can be used as a guide:

The following describes two ways in which PSNTs are utilized:

- First-Party PSNT – established with the beneficiary’s own funds from a personal injury award, workers’ compensation claim, inheritance, savings, or Social Security back payment. The trust is irrevocable and is used for the sole benefit of the disabled individual.

- Medicare Set-Aside (MSA) First-Party PSNT – a PSNT account with an MSA nested within. Established with funds from a workers’ compensation claim or liability lawsuit, the PSNT account transfers the allocated amount to an MSA provider, but retains ownership of the MSA account. These accounts should be considered when a client is dual eligible for both Medicaid and Medicare (or reasonably expected to receive Medicare in the near future) to meet the requirements of the “Secondary Payor” regulations governing Medicare recipients and also the rules for public benefits entitlement.

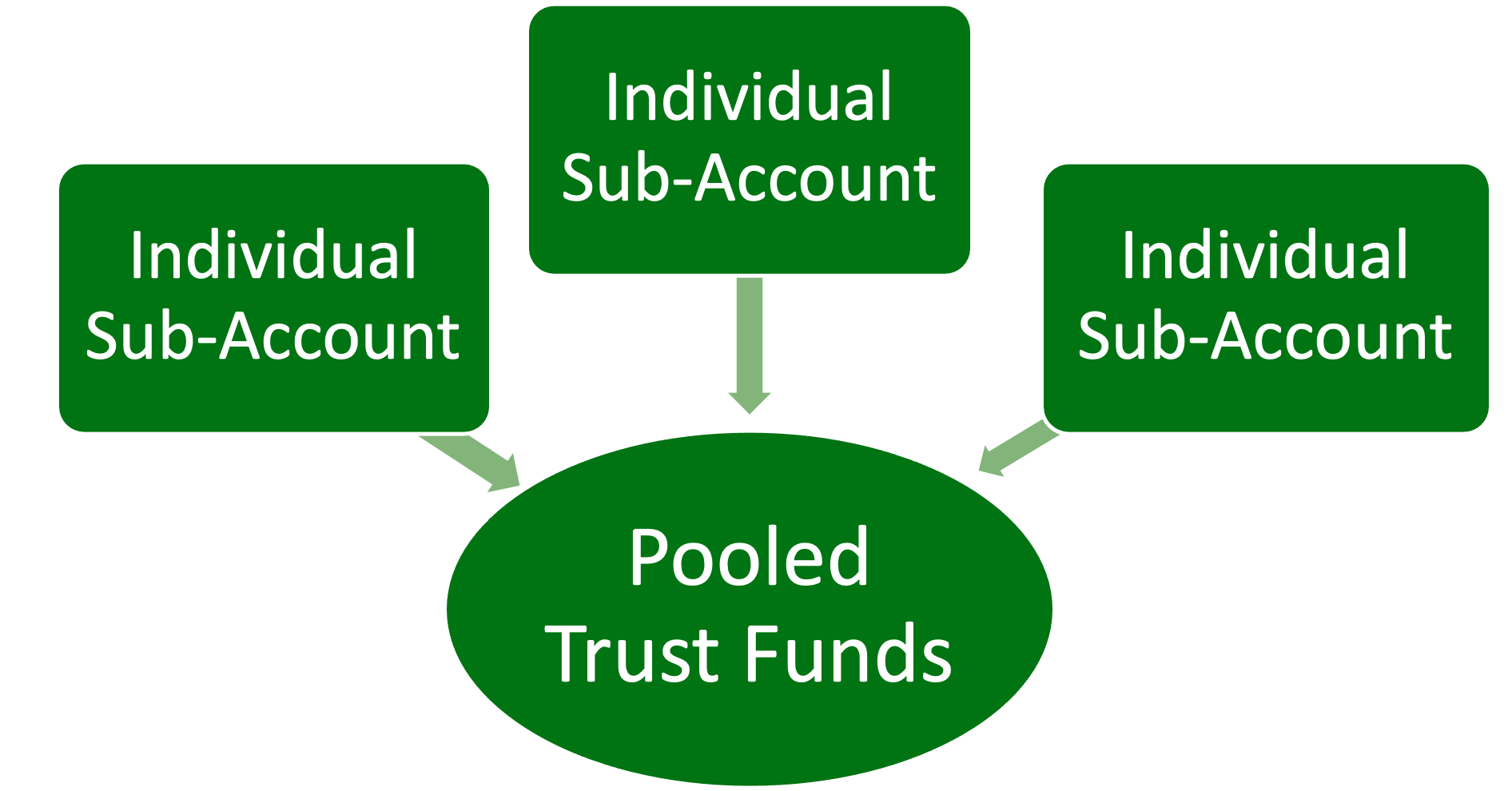

How Pooled Funds are Managed and Invested

Trust funds are “pooled” together for investment purposes, offering lower administrative fees and the potential for greater growth opportunity. Individual sub-accounts are maintained for each beneficiary, and all earnings based on a beneficiary’s share of the principal are reinvested into each sub-account. The beneficiary, or the beneficiary’s advocate, should have access to account information online or via financial statements sent on a regular schedule.

PSNTs serve beneficiaries of varying account sizes from modest settlements to those of more substantial amounts. Funding can be a lump-sum or part of a structured settlement. It is not unusual for a bank or other financial institution to require a minimum of $350,000 to $500,000 to fund a trust. A nonprofit organization, on the other hand, may only require a minimum of $5,000 to fund a PSNT.

Setting Up a PSNT

Each grantor joins the pooled trust and agrees to the terms of the Master Trust Agreement by completing a Joinder Agreement, the legal document to join the PSNT. The Master Trust Agreement allows the nonprofit organization to administer the pooled trust and sets out the terms of that administration.

To serve clients properly, trust administrators have the expertise to make disbursement decisions and understand the rules set forth by the Social Security Administration (SSA) and Medicaid offices in each state. Disbursements from the trust are for the sole benefit of the beneficiary. The following are examples of what a PSNT can be used for:

- Medication and devices

- Assistive technology

- Home modifications, repairs, and upkeep

- Transportation

- Education expenses

- Caregiver expenses

- Pre-need burial and funeral expenses

Remainder Policy

Funds remaining in the account, upon the death of a beneficiary who received Medicaid, are subject to repayment to the state(s) for medical bills paid during the beneficiary’s lifetime. Federal law allows the nonprofit organization to retain the remainder for its charitable purposes in lieu of this repayment, but not all do. Some only retain in the instance that successor beneficiaries would not receive any remainder, and some retain all. Since the policies of individual PSNTs differ, it is important to check with each one to understand its remainder policy completely.

Structured Settlements

Weaving a structured settlement into a PSNT provides tax advantages and future financial security for the beneficiary. The structure can be funded by the defendant’s insurance company, but most companies assign that liability by purchasing annuities to make the payments. Assignments must be done pursuant to IRS Code Section 130 to “qualify,” and these qualified assignments, which are irrevocable, must be done at the time of settlement.

Annuity payments should be made payable to a PSNT and not to the beneficiary as that can cause ineligibility for benefits during the period of the annuity payments. The contingent or successor payee should also be the PSNT to satisfy the Medicaid repayment requirement. A commutation clause which provides for a lump-sum payment to the SNT at the beneficiary’s death should be included as part of the annuity contract. Receiving the commuted value of the remainder allows for orderly administration of the trust including timely repayment to states and immediate payment to successor beneficiaries of remaining assets.

Summary

Setting up a PSNT can alleviate stress by providing individuals with a cost-effective framework for money management. The second article of this two-part series will explore the advantages of nesting an MSA account inside a First-Party PSNT.

Related Articles: